Summary : Communications approaches that will help you effectively reach your employees and encourage behaviors that advance your strategy and improve your results. Some of the key points include:

Keep the message simple

Share market and customer insights to drive behavior

Use a formal framework to inspire, educate and reinforce your ideas

Communicate clearly, consistently, and frequently

Use multiple channels of communication

Speak to your audience and in their language

Make use of storytelling to fully engage employees emotions

Commit the resources necessary to help employees internalize our strategy

Marketing takes time, money, and preparation. One of the best ways to stay on schedule and on budget is to make a marketing plan. It describes the actions you’ll take to persuade potential customers to buy your products or services.

Your business plan should contain the central elements of your marketing strategy. Your marketing plan turns your strategy into action.

Use these sections in your marketing plan

Most marketing plans cover these topics. As always, use what works best for your business.

Target market

Describe your audience in detail. Look at the market’s size, demographics, unique traits, and trends that relate to demand for your business.

Competitive advantage

Describe what gives your product or service an advantage over the competition. It might be a better product, a lower price, or an excellent customer experience. Sometimes, an environmentally friendly certification or “made in the USA” on your label can be an important factor for customers.

Sales plan

Describe how you’ll literally sell your service or product to your customers. List the sales methods you’ll use, like retail, wholesale, or your own online store. Explain each step your customer takes once they decide to buy.

Marketing and sales goals

Describe your marketing and sales goals for the next year. Common marketing and sales goals are to increase email subscribers, grow market share, or increase sales by a certain percent.

Marketing action plan

Describe how you’ll achieve your marketing and sales goals. List marketing channels you’ll use, like online advertising, radio ads, or billboards. Explain your pricing strategy and how you’ll use promotions. Talk about the customer support that happens after the sale. The federal government regulates advertising and labeling for a number of consumer products, so make sure your advertising is legally compliant.

Budget

Include a complete breakdown of the costs of your marketing plan. Try to be as accurate as possible. You’ll want to keep tracking your costs once you put your plan into action.

Target market

Competitive advantage

Sales plan

Marketing and sales goals

Marketing action plan

Budget

Measure and update your plan

Plan to compare your marketing and sales costs to the revenue it generates. You want to make sure you’re getting a positive return on investment, or ROI.

Some tactics are hard to measure — like print advertising or word-of-mouth campaigns. Get creative and use others’ advice, but be consistent in how you measure the effectiveness of your marketing efforts.

Marketing plans should be maintained on an annual basis, at minimum. Measuring ROI will help you know which part of the plan is working and which part needs to be updated.

Don’t forget about operations

Spread the word

John and Kelly developed a marketing plan to persuade potential customers to visit their auto repair shop.

Not everyone agrees on the exact distinctions between marketing and sales, but most people recognize they’re connected. The influence operations has on marketing and sales is often overlooked.

Simple operations elements like your staff uniform, where your product is made, or the product return process contribute to your customer’s experience. That experience shapes how your customers view your company, and can influence whether they’ll become a loyal customer for life or tell their friends to stay away.

Choose how you’ll accept payments

The kinds of payments you accept can impact your marketing and sales, as well as your bottom line. Accept forms of payments that are cost effective, secure, and provide a positive experience for your customers.

To accept credit and debit cards, you’ll need either a merchant services account with a bank or an account with an independent payment processing company.

You’ll pay small processing fees for each credit or debit card transaction, plus costs for setting up any necessary equipment.

Accepting credit and debit cards exposes you to the risk of fraud, but most vendors provide a certain level of protection for your business. Make sure that you use an EMV chip reader, which will limit both fraud and your liability.

Checks

You only need a business bank account to accept checks.

You’ll want to create a policy for accepting checks to help you avoid bad or fraudulent checks. Standard practices include only taking checks from well-known or in-state banks, or requiring checks be only for the exact amount owed. You could also use a third party service to help verify the quality of the check.

If a check bounces, your options to get the final payment will vary depending on your location. Some states require businesses to mail a registered letter and allow a designated waiting period to lapse before further action is taken. To get payment for a bounced check, you could end up in small claims court or using a collection agency.

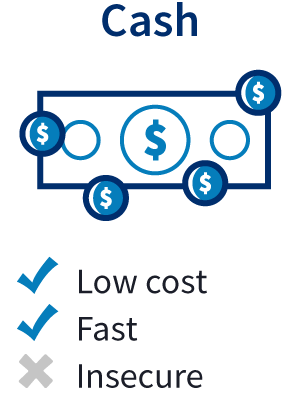

Cash

Many small businesses operate as “cash only” merchants because it’s fast, easy, and inexpensive.

If you accept cash, remember that large sums of cash can add to accounting time and come with an additional security risk. You’ll want a secure way to hold your cash, like a register and a safe.

There are special reporting requirements for cash. The IRS requires you to report if your business gets more than $10,000 in cash, or a cash equivalent, from one buyer as a result of a single transaction or two or more related transactions.

Online payments

If you sell your product or service online, you could accept payment through your website with an online payment service.

Online payment services typically accept credit and debit cards in addition to other popular online money transfer services. You’ll pay fees to in order to accept payments online, just like accepting credit cards in a physical location.

Online payment services require a virtual shopping cart to calculate the total, tax, and shipping costs of an order, in addition to collecting customer account and shipping information. Some online payment service providers offer free shopping cart services to businesses.

Establish a basic payroll structure to help you hire employees. Then, manage employees properly with a general understanding of state and federal labor laws.

Decide if you want an independent contractor or an employee

Ensure new employees return a completed W-4 form

Schedule pay periods to coordinate tax withholding for IRS

Create a compensation plan for holiday, vacation and leave

Choose an in-house or external service for administering payroll

Decide who will manage your payroll system

Know which records must stay on file and for how long

Report payroll taxes as needed on quarterly and annual basis

The IRS maintains the Employer’s Tax Guide, which provides guidance on all federal tax filing requirements that could apply to the obligations for your small business. Check with your state tax agency for employer filing stipulations.

Employees and independent contractors

Distinguishing between employees and independent contractors can impact your bottom line, as this affects how you withhold taxes and avoid costly legal consequences. Learn the differences before hiring your first employee.

An independent contractor operates under a separate business name from your company and invoices for work completed. Independent contractors can sometimes qualify as employees in a legal sense. The Equal Employment Opportunity Commission created a guide for making the determination.

If your contractor is discovered to meet the legal definition of employee, you may need to pay back taxes and penalties, provide benefits, and reimburse for wages stipulated under the Fair Labor Standards Act.

Employees

Independent contractors

Plan to offer employee benefits

Healthcare and other benefits play a significant role in hiring and retaining employees. Some employee benefits are required by law, but others are optional.

Required employee benefits

Social Security taxes: Employers must pay Social Security taxes at the same rate as their employees

Unemployment insurance: Varies by state, and you may need to register with your state workforce agency

Optional employee benefits

Your small businesses can offer a complete range of optional benefits to help attract and retain employees. Even if a benefit you offer is optional, it might still have to comply with certain laws if you choose to offer it.

Employees can expand coverage through the Affordable Care Act and some may qualify for benefits via the Consolidated Omnibus Budget Reconciliation Act (COBRA). Businesses must extend the option of COBRA benefits to employees who are terminated or laid off.

Retirement plans are a very popular employee benefit. Consider offering an employer-sponsored plan like a 401k or a pension plan. The federal government offers a wide range of resources to aid small business owners in choosing their retirement plan and pension.

Employee incentive programs

Employee incentive programs can boost morale and create more draw for open positions: Common incentives such as stock options, flex time, wellness programs, corporate memberships and company events.

Consider benefits administration software if your budget allows. It can make your accounting easier and more efficient. Detailing these benefits in the employee handbook helps your staff make decisions, and they can use it as a reference for workplace requirements.

Follow federal and state labor laws

Protect workers’ rights and your business by adhering to labor laws, which means you must ensure that business practices align with industry regulations.

Let’s see what Jack and Kathy did so that they could hire employees to help manage the day-to-day operation of their bicycle shop.

Jack and Kathy need to establish a payroll structure to hire employees to work at their bicycle shop.

So they wrote descriptions for each position they wanted to fill — clearly defining the responsibilities of each role and the qualifications needed — and posted the openings on popular job boards online.

Jack and Kathy set wages for each position, at least meeting their state’s minimum wage requirement.

Once hired, each new employee completed a W-4 form, which Jack and Kathy submitted to the I.R.S. (The IRS requires businesses to keep records of employment taxes for at least four years.) They also completed Form I-9, which requires Jack and Kathy to examine documents to confirm the employee’s citizenship or eligibility to work in the U.S. (They don’t have to submit this form to the federal government, but they do have to keep them on file.)

Jack and Kathy contacted their state tax office to learn about their state tax obligations. They also reported their new employees to their state directory within 20 days of the employee hire date, as required by their state.

Jack and Kathy paid for an online payroll service, which automatically calculates how much their employees should be paid each pay period, accounting for tax deductions.

Jack and Kathy have hired employees, have a system in place to pay their employees, and have prepared the required tax records and reports .

Accounting for revenue and expenses can help keep your business running smoothly. Make sure you maintain proper bookkeeping and have a basic knowledge of business finances.

The balance sheet is the foundation of managing your finances. It operates as a snapshot of your business financials. It helps you keep track of your capital and provide a cash flow projection for future years.

A balance sheet will help you account for costs like employees and supplies. It will also help you track assets, liabilities, and equity. You can get insights by separating and analyzing segments of your business, like comparing online sales to face-to-face sales.

Cost-benefit analysis (CBA)

Looking closely at money-in and money-out helps maintain a sustainable balance between profit and loss. From development and operations to recurring and nonrecurring costs, it’s important to categorize expenses in your balance sheet. Then, you can use a cost-benefit analysis to weigh the strengths and weaknesses of a business decision, and put potential recurring benefits and cost reductions in context.

A CBA is a technique for making non-critical choices in a relatively quick and easy way. It simply involves adding money in benefits and money in costs over a specified time period, before subtracting costs from benefits to determine success in terms of dollars. This can come in handy with hiring another employee or an independent contractor.

For example, let’s say you’re deciding whether to add outdoor seating for your sausage themed restaurant, Haute Dog. You estimate outdoor seating would add $5,000 in extra profit from sales each year. But, the outdoor seating permit costs $1,000 each year, and you’d also have to spend $2,000 to buy outdoor tables and chairs. Your cost-benefit analysis shows that you should add outdoor seating, because the new benefits ($5,000 in new sales) outweigh the new costs ($3,000 in permitting and equipment expenses).

Pick a method of accounting

Businesses often use either the accrual or cash methods of recording purchases. The accrual method puts transactions on the books immediately upon completing the sale. The cash method only records this once payment has been received.

For example, if you make a sale in January and receive the $200 payment in February, an accrual method would allow you to record that on January’s books, while the cash method would require that payment to land on February’s books.

Method

Pros

Cons

Accrual

Creates immediate snapshot. Can reduce tax burden.

More complex to manage. Potentially deceiving figures.

Cash

Shows cash flow clearly. Easier to understand.

Limits predictive value. Less long-term clarity.

GAAP

There are many strategies for preparing financial statements for a small business. Generally accepted accounting principles, known as GAAP or “Gap,” provides a common a way to standardize financial reporting using the accrual method. Private companies aren’t required to follow GAAP. The Financial Accounting Standards Board (FASB) maintains GAAP in the United States.

Get accounting help

You might want to get help with your accounting. Consider hiring a certified public accountant (CPA), bookkeeper, or using an online service.

A CPA will typically cost more than online services, but can normally offer more tailored service for your specific business needs. A bookkeeper can provide basic day-to-day functions at a lower cost, but won’t possess the formal accounting education of a CPA.

Establishing and managing business credit can help your company secure financing when you need it, and with better terms. Business credit can be crucial for negotiating supply agreements and protecting against business identity theft.

These five steps can lay the groundwork to sound financial planning.

Determine whether you have business credit on file with Dun & Bradstreet

Establish a business credit history by using lines of credit associated with your business

Pay bills on time and understand other factors that influence your credit rating

Keep your credit files current and monitor for ratings changes

Know your customers’ and vendors’ credit standing

Knowing your customers’ credit standing gives you a window into consumer patterns, and that can affect your marketing and sales strategy. You may not need to conduct credit checks, but there are credit evaluation tools available for small business. Customer behavior also impacts your business’s cash flow, which affects planning for future supplies, hiring employees, and expanding your business.

The business structure you choose influences everything from day-to-day operations, to taxes, to how much of your personal assets are at risk. You should choose a business structure that gives you the right balance of legal protections and benefits.

Choose carefully. While you may convert to a different business structure in the future, there may be restrictions based on your location. This could also result in tax consequences and unintended dissolution, among other complications.

Consulting with business counselors, attorneys, and accountants can prove helpful.

Review common business structures

Sole proprietorship

A sole proprietorship is easy to form and gives you complete control of your business. You’re automatically considered to be a sole proprietorship if you do business activities but don’t register as any other kind of business.

Sole proprietorships do not produce a separate business entity. This means your business assets and liabilities are not separate from your personal assets and liabilities. You can be held personally liable for the debts and obligations of the business. Sole proprietors are still able to get a trade name. It can also be hard to raise money because you can’t sell stock, and banks are hesitant to lend to sole proprietorships.

Sole proprietorships can be a good choice for low-risk businesses and owners who want to test their business idea before forming a more formal business.

Partnership

Partnerships are the simplest structure for two or more people to own a business together. There are two common kinds of partnerships: limited partnerships (LP) and limited liability partnerships (LLP).

Limited partnerships have only one general partner with unlimited liability, and all other partners have limited liability. The partners with limited liability also tend to have limited control over the company, which is documented in a partnership agreement. Profits are passed through to personal tax returns, and the general partner — the partner without limited liability — must also pay self-employment taxes.

Limited liability partnerships are similar to limited partnerships, but give limited liability to every owner. An LLP protects each partner from debts against the partnership, they won’t be responsible for the actions of other partners.

Partnerships can be a good choice for businesses with multiple owners, professional groups (like attorneys), and groups who want to test their business idea before forming a more formal business.

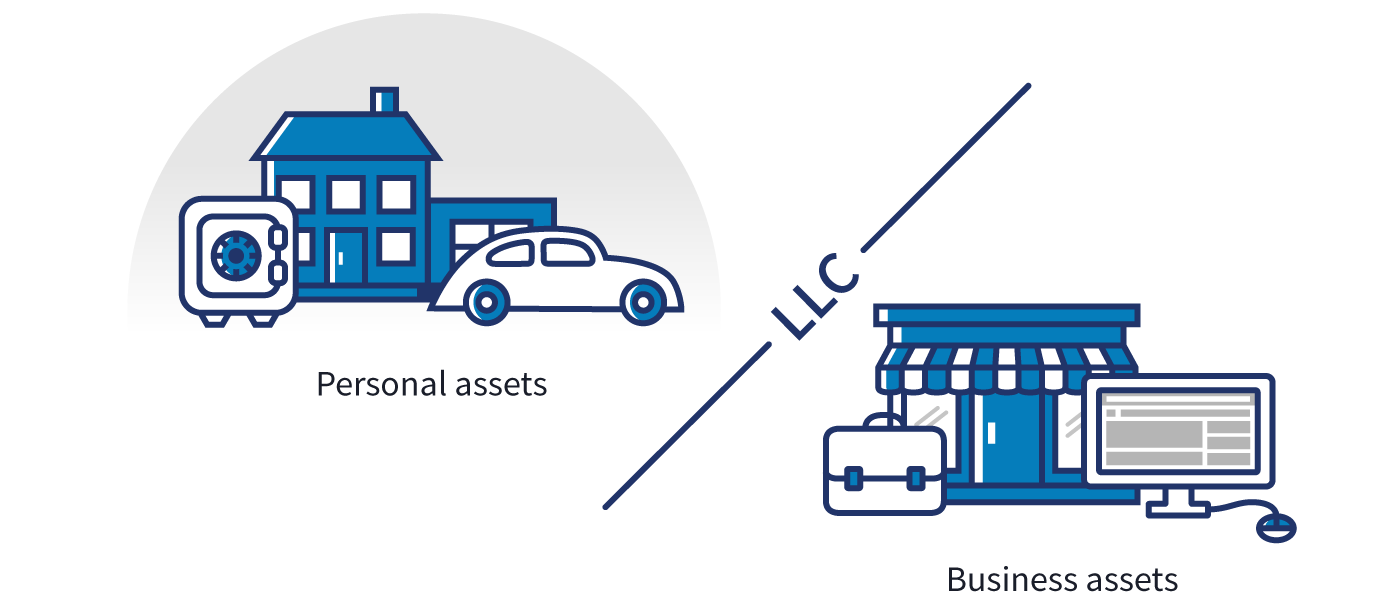

Limited liability company (LLC)

An LLC lets you take advantage of the benefits of both the corporation and partnership business structures.

LLCs protect you from personal liability in most instances, your personal assets — like your vehicle, house, and savings accounts — won’t be at risk in case your LLC faces bankruptcy or lawsuits.

Profits and losses can get passed through to your personal income without facing corporate taxes. However, members of an LLC are considered self-employed and must pay self-employment tax contributions towards Medicare and Social Security.

LLCs can have a limited life in many states. When a member joins or leaves an LLC, some states may require the LLC to be dissolved and re-formed with new membership — unless there’s already an agreement in place within the LLC for buying, selling, and transferring ownership.

LLCs can be a good choice for medium- or higher-risk businesses, owners with significant personal assets they want to be protected, and owners who want to pay a lower tax rate than they would with a corporation.

Corporation

C corp

A corporation, sometimes called a C corp, is a legal entity that’s separate from its owners. Corporations can make a profit, be taxed, and can be held legally liable.

Corporations offer the strongest protection to its owners from personal liability, but the cost to form a corporation is higher than other structures. Corporations also require more extensive record-keeping, operational processes, and reporting.

Unlike sole proprietors, partnerships, and LLCs, corporations pay income tax on their profits. In some cases, corporate profits are taxed twice — first, when the company makes a profit, and again when dividends are paid to shareholders on their personal tax returns.

Corporations have a completely independent life separate from its shareholders. If a shareholder leaves the company or sells his or her shares, the C corp can continue doing business relatively undisturbed.

Corporations have an advantage when it comes to raising capital because they can raise funds through the sale of stock, which can also be a benefit in attracting employees.

Corporations can be a good choice for medium- or higher-risk businesses, businesses that need to raise money, and businesses that plan to “go public” or eventually be sold.

S corp

An S corporation, sometimes called an S corp, is a special type of corporation that’s designed to avoid the double taxation drawback of regular C corps. S corps allow profits, and some losses, to be passed through directly to owners’ personal income without ever being subject to corporate tax rates.

Not all states tax S corps equally, but most recognize them the same way the federal government does and taxes the shareholders accordingly. Some states tax S corps on profits above a specified limit and other states don’t recognize the S corp election at all, simply treating the business as a C corp.

There are special limits on S corps. S corps can’t have more than 100 shareholders, and all shareholders must be U.S. citizens.You’ll still have to follow strict filing and operational processes of a C corp.

S corps also have an independent life, just like C corps. If a shareholder leaves the company or sells his or her shares, the S corp can continue doing business relatively undisturbed.

S corps can be a good choice for a businesses that would otherwise be a C corp, but meet the criteria to file as an S corp.

B corp

A benefit corporation, sometimes called a B corp, is a for-profit corporation recognized by a majority of U.S. states. B corps are different from C corps in purpose, accountability, and transparency, but aren’t different in how they’re taxed.

B corps are driven by both mission and profit. Shareholders hold the company accountable to produce some sort of public benefit in addition to a financial profit. Some states require B corps to submit annual benefit reports that demonstrate their contribution to the public good.

There are several third-party B corp certification services, but none are required for a company to be legally considered a B corp in a state where the legal status is available.

Close corporation

Close corporations resemble B corps but have a less traditional corporate structure. These shed many formalities that typically govern corporations and apply to smaller companies.

State rules vary, but shares are usually barred from public trading. Close corporations can be run by a small group of shareholders without a board of directors.

Nonprofit corporation

Nonprofit corporations are organized to do charity, education, religious, literary, or scientific work. Because their work benefits the public, nonprofits can receive tax-exempt status, meaning they don’t pay state or federal taxes income taxes on any profits it makes.

Nonprofit corporations need to follow organizational rules very similar to a regular C corp. They also need to follow special rules about what they do with any profits they earn. For example, they can’t distribute profits to members or political campaigns.

Nonprofits are often called 501(c)(3) corporations — a reference to the section of the Internal Revenue Code that is most commonly used to grant tax-exempt status.

Cooperative

A cooperative is a business or organization owned by and operated for the benefit of those using its services. Profits and earnings generated by the cooperative are distributed among the members, also known as user-owners. Typically, an elected board of directors and officers run the cooperative while regular members have voting power to control the direction of the cooperative. Members can become part of the cooperative by purchasing shares, though the amount of shares they hold does not affect the weight of their vote.

Combine different business structures

Designations like S corp and nonprofit aren’t strictly business structures — they can also be understood as a tax status. It’s possible for an LLC to be taxed as a C corp, S corp, or a nonprofit. These arrangements are far less common and can be more difficult to setup. If you’re considering one of these non-standard structures, you should speak with a business counselor or an attorney to help you decide.

Compare business structures

Compare the general traits of these business structures, but remember that ownership rules, liability, taxes, and filing requirements for each business structure can vary by state.

Business structure

Ownership

Liability

Taxes

Sole proprietorship

One person

Unlimited personal liability

Personal tax only

Partnerships

Two or more people

Unlimited personal liability unless structured as a limited partnership

Self-employment tax (except for limited partners) Personal tax

Limited liability company (LLC)

One or more people

Owners are not personally liable

Self-employment tax Personal tax or corporate tax

Corporation – C corp

One or more people

Owners are not personally liable

Corporate tax

Corporation – S corp

One or more people, but no more than 100, and all must be U.S. citizens

Owners are not personally liable

Personal tax

Corporation – B corp

One or more people

Owners are not personally liable

Corporate tax

Corporation – Nonprofit

One or more people

Owners are not personally liable

Tax-exempt, but corporate profits can’t be distributed

Find an investor for your business through a Small Business Investment Company (SBIC) licensed by the Small Business Administration (SBA).

SBICs invest in small businesses

An SBIC is a privately owned company that’s licensed and regulated by the SBA. SBICs invest in small businesses in the form of debt and equity. The SBA doesn’t invest directly into small businesses, but it does provide funding to qualified SBICs with expertise in certain sectors or industries. Those SBICs then use their private funds, along with SBA-guaranteed funding, to invest in small businesses.

What you can get

SBICs invest in small businesses through debt, equity, or a combination of both. Debt is a loan an SBIC gives to a business, which the business must pay back, along with any interest. Equity is a share of ownership an SBIC gets in a business in exchange for providing funding. Sometimes, an SBIC invests in a business through both debt and equity. Such an investment includes both loans and shares of ownership. A typical SBIC investment is made over a 3-year period.

Debt

A typical SBIC loan ranges from $250,000 to $10 million, with an interest rate between 9% and 16%.

Equity

SBICs will invest in your business in exchange for a share of ownership in your company. Typical investments range from $100,000 to $5 million.

Debt with equity

Financing includes loans and ownership shares. Loan interest rates are typically between 10% and 14%. Investments range from $250,000 to $10 million.

Check your eligibility

SBICs typically target mature, profitable businesses with sufficient cashflow to pay interest. However, each SBIC has its own investment profile in terms of targeted industry, geography, company maturity, and the types and size of financing they provide. There are a few universal requirements.

Be a U.S. business

At least 51% of your employees and assets must be within the U.S.

Be a small business

Qualify as a small business according to SBA size standards.

Be in an approved industry

Farmland, real estate, and financing are some of the industries that don’t qualify.

If your small business is interested in SBIC financing, take the following steps when you approach an SBIC.

If your small business is interested in SBIC financing, take the following steps when you approach an SBIC.

1. Research an SBIC

Find an SBIC using our online directory, and make sure they’re actively investing in businesses in your region, size, and industry.

2. Prepare your business plan

Get ready to make the case that investing in your business would be profitable for the SBIC.

3. Contact an SBIC

For the best chance to get financing, use your network. Talk to accountants, attorneys, and executives to get an introduction to an SBIC. See a directory of SBICs.

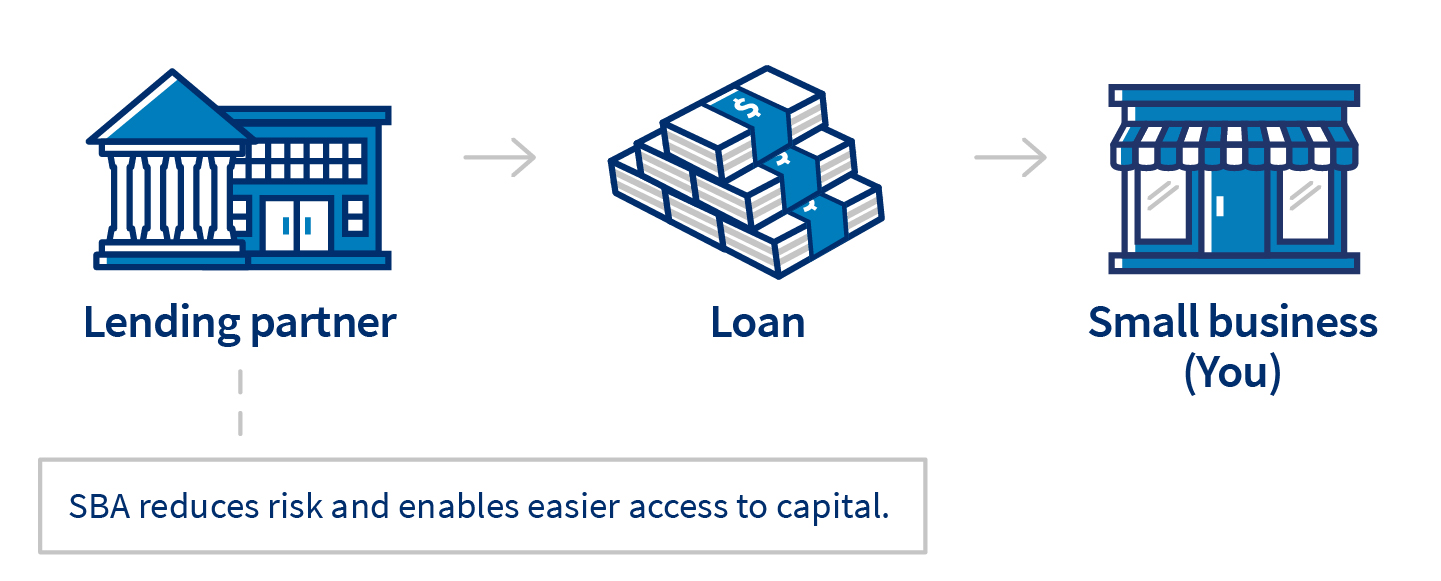

The SBA works with lenders to provide loans to small businesses. The agency doesn’t lend money directly to small business owners. Instead, it sets guidelines for loans made by its partnering lenders, community development organizations, and micro-lending institutions. The SBA reduces risk for lenders and makes it easier for them to access capital. That makes it easier for small businesses to get loans.

Benefits of SBA-guaranteed loans

Competitive terms

SBA-guaranteed loans generally have rates and fees that are comparable to non-guaranteed loans.

Counseling and education

Some loans come with continued support to help you start and run your business.

Unique benefits

Lower down payments, flexible overhead requirements, and no collateral needed for some loans.

Stay safe

Protect yourself from predatory lenders by looking for warning signs.

Get $500 to $5.5 million to fund your business

Loans guaranteed by the SBA range from small to large and can be used for most business purposes, including long-term fixed assets and operating capital. Some loan programs set restrictions on how you can use the funds, so check with an SBA-approved lender when requesting a loan. Your lender can match you with the right loan for your business needs.

Working capital

Like seasonal financing, export loans, revolving credit, and refinanced business debt.

Fixed assets

Like furniture, real estate, machinery, equipment, construction, and remodeling.

Eligibility requirements

Lenders and loan programs have unique eligibility requirements. In general, eligibility is based on what a business does to receive its income, the character of its ownership, and where the business operates. Normally, businesses must meet size standards, be able to repay, and have a sound business purpose. Even those with bad credit may qualify for startup funding. The lender will provide you with a full list of eligibility requirements for your loan.

Be a for-profit business

The business is officially registered and operates legally.

Do business in the U.S.

The business is physically located and operates in the U.S. or its territories.

Have invested equity

The business owner has invested their own time or money into the business.

Exhaust financing options

The business cannot get funds from any other financial lender.

Starting a business involves planning, making key financial decisions, and completing a series of legal activities. Scroll down to learn about each step.

1.) Conduct market research

Market research will tell you if there’s an opportunity to turn your idea into a successful business. It’s a way to gather information about potential customers and businesses already operating in your area. Use that information to find a competitive advantage for your business.

2.) Write your business plan

Your business plan is the foundation of your business. It’s a roadmap for how to structure, run, and grow your new business. You’ll use it to convince people that working with you — or investing in your company — is a smart choice.

3.) Fund your business

Your business plan will help you figure out how much money you’ll need to start your business. If you don’t have that amount on hand, you’ll need to either raise or borrow the capital. Fortunately, there are more ways than ever to find the capital you need.

4.) Pick your business location

Your business location is one of the most important decisions you’ll make. Whether you’re setting up a brick-and-mortar business or launching an online store, the choices you make could affect your taxes, legal requirements, and revenue.

5.) Choose a business structure

The legal structure you choose for your business will impact your business registration requirements, how much you pay in taxes, and your personal liability.

6.) Choose your business name

It’s not easy to pick the perfect name. You’ll want one that reflects your brand and captures your spirit. You’ll also want to make sure your business name isn’t already being used by someone else.

7.) Register your business

Once you’ve picked the perfect business name, it’s time to make it legal and protect your brand. If you’re doing business under a name different than your own, you’ll need to register with the federal government, and maybe your state government, too.

8.) Get federal and state tax IDs

You’ll use your employer identification number (EIN) for important steps to start and grow your business, like opening a bank account and paying taxes. It’s like a social security number for your business. Some — but not all — states require you to get a tax ID as well.

9.) Apply for licenses and permits

Keep your business running smoothly by staying legally compliant. The licenses and permits you need for your business will vary by industry, state, location, and other factors.

10.) Open a business bank account

A small business checking account can help you handle legal, tax, and day-to-day issues. The good news is it’s easy to set one up if you have the right registrations and paperwork ready.

You must be logged in to post a comment.